How do rising mortgage rates affect housing affordability?

With inflation rising at a fast pace, everyday life is becoming more expensive. To counter inflation, the Fed announced an interest rate increase of half a percentage point, the highest increase since 2000. In expectation of this rise, and after the announcement itself, we have seen a steady rise in mortgage rates. According to Freddie Mac, 30-year fixed rates in the US were on average 5.27% last week, a 2.31 percentage point increase relative to a year before. (see Figure 1) The bank of England approved a 25 basis point increase, and the ECB is likely to raise rates as of July, for both of these institutions the first-time increase in over a decade. As a result of these (anticipated) changes, we also see mortgage rates increasing sharply in these areas.

Housing prices have been steadily increasing in the last decade, mainly caused by a low-interest-rate environment and a supply shortage. Now that one of these factors is changing, messages arise about a potential slowdown of the market, creating a spark of hope for prospective homebuyers. However, how likely is this to happen, and is this contributing to housing affordability for future buyers?

Although a slowdown seems a positive development for prospective homebuyers at first, we should not forget the cause of the slowdown. With rising mortgage rates, monthly mortgage payments become more expensive. As a result, keeping income equal, the amount of mortgage that a household can take out decreases. This is first going to affect new home buyers and current mortgage holders under a flexible interest rate.

Next to that, general living costs are increasing and economic growth, e.g. income, is not catching up (stagflation). This leaves less room for households to spend, and can negatively affect the maximum mortgage amount that they can afford. The question of whether the current situation will be beneficial for future buyers depends on the relative strengths of the two effects: higher monthly mortgage payments, and the decrease or slowdown in asking prices.

Given the current real estate market, prices are unlikely to drop rapidly. Although demand surplus may decrease, there is still an overwhelming demand given the current supply. Supply can partially increase in the short run because of homeowners that want to sell their houses at current prices and under higher uncertainty, but both of these factors are likely to be small given the current disbalance in the market.

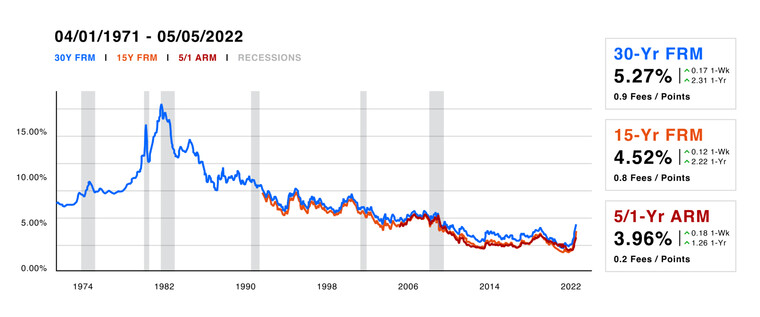

On another note, it is important to put the current mortgage rates into a historical perspective. If we regard mortgage terms over a longer time stretch (as depicted in figure 2), we can say that the rates are actually still relatively low. This is also a consideration to take into account when considering a fixed or floating mortgage rate.

Overall, the development of the mortgage rate and its effect on the housing market seems to be another letdown for prospective homebuyers. Whether this is a good moment to buy or sell, and what mortgage terms to accept is dependent on expectations about multiple developments. It is important to closely follow current inflation drivers, such as the Ukraine war and Chinese lockdowns, as well as its interplay with monetary policy.